Jersey Oil & Gas (JOG):

Target Price: 750p (from 800p)

JOG is a UK E&P focused on its operated Greater Buchan Area (GBA) development project. The company has made significant progress increasing its understanding of the subsurface and scoping out the development concept, all leading into a now-commenced farm out process. Success would secure project progress, bringing additional funding and industry endorsement, and act as a material catalyst. The company has raised (March 17) £15m of equity at 165p via a placing to maintain ongoing GBA momentum ahead of securing a farm out

GBA a significant UK development. JOG holds 100% of its GBA project, with the core development incorporating 162mmboe of 2C economic resource, with additional exploration prospects. Sustained progression should draw increasing levels of industry and stock market attention.

The farm out process is a key catalyst. The company recently launched its GBA farm out process, an important moment that should secure development progression and industry endorsement. Success here would be a significant 2021 catalyst.

Equity Raise

The equity raise supports project and farm out. The £15m placing will allow JOG to maintain project momentum, including entering FEED, to maintain project timelines and support the farm out process.

The valuation implies substantial upside potential. An 850p total risked NAV implies that the GBA project is significantly undervalued by the market. Success in the farm out process could go a long way to helping reduce this discount.

Potential positive upcoming catalysts include the GBA farm out process – commenced Q1 2021. This should close before the end of 2021, with the potential for a deal announcement some time in mid-2021. There is also GBA FEED work, scheduled to start in H2 2021, with potential GBA exploration wells confirmation in this timeframe as well.

Further timelines include GBA development FID in the second half of next year with potential GBA exploration wells – Q2 2023. We should receive GBA development updates from late 2022 onwards and the GBA first oil itself in 2025.

Valuation

The primary valuation method for E&P companies is building DCF models asset by asset, and then combining these to create a sum-of-the-parts NAV, adjusting for net debt/cash and other corporate items.

The model for JOG returns a total risked NAV of 850p/share risked, going to 1,713p/share unrisked, using a US$65m long-term Brent assumption and assuming 70% JOG interest to try and account for the farm out. These numbers represent a change to Arden’s previously published valuation due to increased allowance for 2021 CAPEX, alongside updating for the equity raise of £15m at 165p.

The risk / reward against a present 38 million market cap is very high, with a potential to move sharply higher on anticipation of success

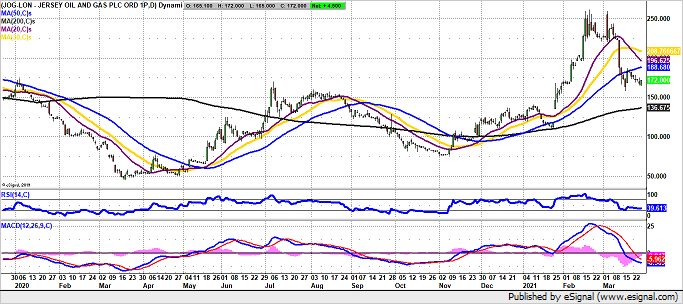

Technical Analysis

The daily chart of JOG indicates support from uptrend line and 100 day moving average, setting a target of 250p in the next month or so in the wake of a hefty gap higher for the shares through former resistance.

Disclaimer:

Zakmir.com is a purely journalistic website – Zak Mir is a member of the National Union of Journalists. There is no intention here of providing financial advice. It is recommended you seek an independent professional opinion before deciding whether or not to take any action with regard to anything written here.